Global Expansion Support for Japanese Companies

Global Expansion Support for Japanese companies

Problems Facing Japan’s Global Companies

Financial Reporting

Late or missing monthly reporting

Unclear account statements

Delay in local accounting information reaching Japanese accounting audit

Accounting Software

Fewer features

Accounting records that cannot be corrected in real time at the head office in Japan

Communication

Unable to contact local accountant or communicate clearly.

Time-consuming to check with local accountant in foreign language.

Inability to obtain expert advice on local accounting and tax issues.

Language

Time and employee-hours wasted on translation.

Human Resources

Lack of accounting personnel dispatched from Japan.

Recruitment of local personnel who understand Japanese accounting practices.

Tax Risks

Tax Risks Arising from Intangible Assets

Our Solutions

These our solutions solve your problems.

Our Solutions

These our solutions solve your problems.

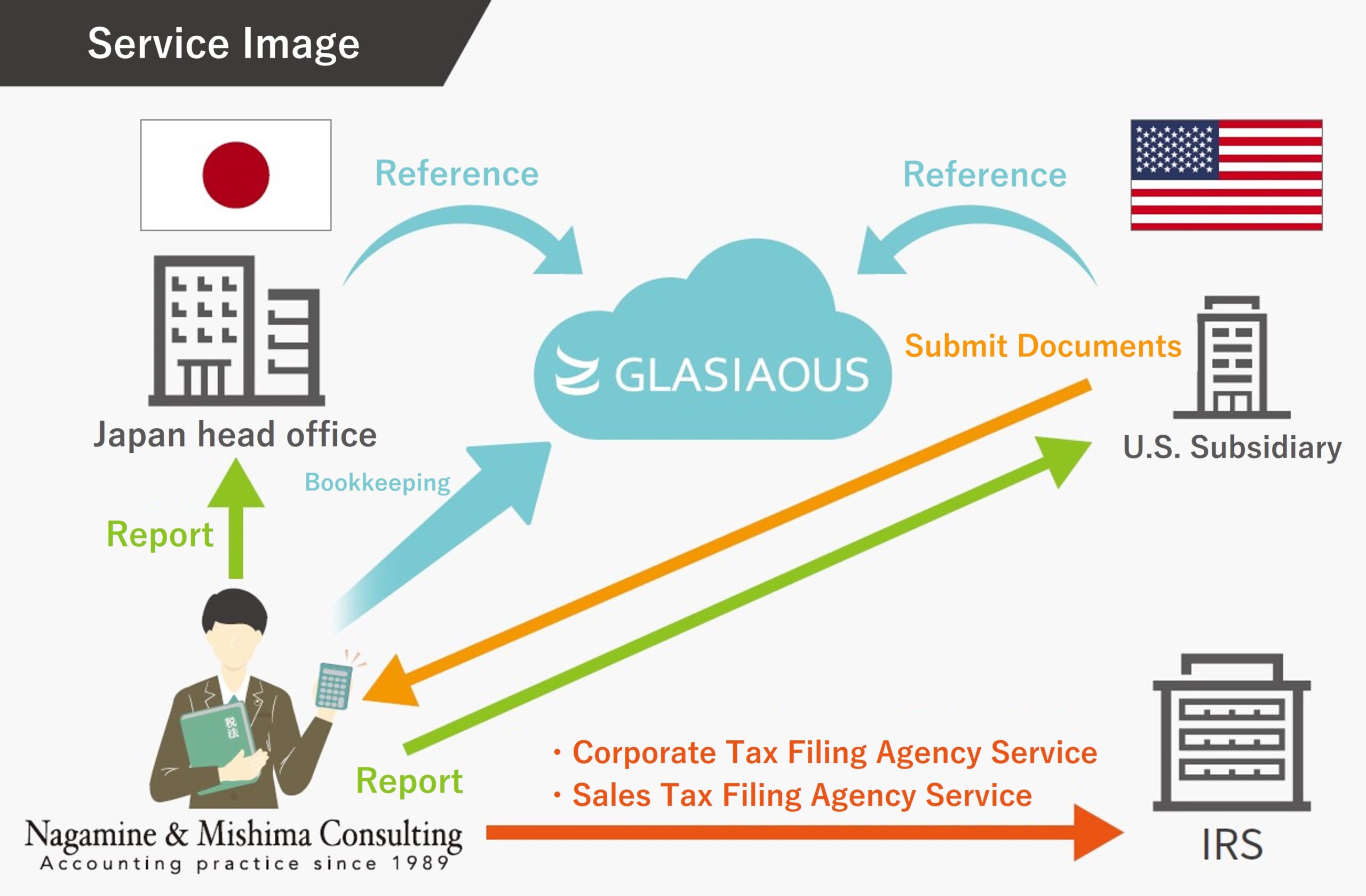

U.S. Subsidiary Bookkeeping & Tax Filing Services

We have launched bookkeeping and U.S. corporate tax compliance services for U.S. subsidiaries of Japanese companies.

A U.S. Certified Public Accountant (CPA) with years of practical experience in the U.S. will support your company and provide comprehensive services, from bookkeeping to corporate tax compliance, tailored to your specific accounting and tax needs in the U.S.

We use the cloud-based international accounting ERP system, ‘GLASIAOUS,’ allowing clients real-time access to detailed accounting data in both Japanese and English.

These services are ideal for small to medium size corporations (SMC) with around 2 to 10 local employees.

Our Japanese staff based in Japan will handle your company’s book keeping, which allows us to offer these services at a lower cost compared to U.S.-based accounting firms. Communication with your parent company can be conducted in Japanese, ensuring a smooth communication.

You can solve your accounting challenges without dispatching your talented personnel or struggling to secure local accounting staff. If you are facing difficulties in securing local accounting staff, please feel free to consult with us.

*We can handle tax filings other than corporate income tax.

*We can refer the local accounting firm which prepares audit or financial statement opinion.

What is “GLASIAOUS”, a Cloud-Based International Accounting ERP System?

Solving your accounting issues with a real-time network of cross-border accounting.

Solving your accounting issues with a real-time network of cross-border accounting.

We provides services using GALSIAOUS, a cloud-based international accounting ERP service which supports multiple languages, multiple currencies, and multiple accounting standards.

The software supports multiple languages and currencies. It can be viewed in Japanese, English, and other languages. Additionally, since it is cloud-based, detailed data can be accessed from anywhere in the world by connecting to the cloud.

Global Network Services

Nagamine & Mishima Consulting (NMC) has been actively building networks with accounting firms around the world since its establishment in 1989.

Currently, NMC is a Japanese member of PRAXITY, an international association of accounting and auditing firms from 102 countries, headquartered in London, and has a network of overseas lawyers and accountants cultivated over the years by our Representative Partner, Mr. Nagamine. Through them, NMC is able to provide tax and accounting services in the USA, Europe and almost the entire world.

In particular, the Moores Rowland Network, of which NMC is a key member, has been established with the Asian countries listed below, enabling the provision of highly detailed services.

Nagamine & Mishima Consulting (NMC) has been actively building networks with accounting firms around the world since its establishment in 1989.

Currently, NMC is a Japanese member of PRAXITY, an international association of accounting and auditing firms from 102 countries, headquartered in London, and has a network of overseas lawyers and accountants cultivated over the years by our Representative Partner, Mr. Nagamine. Through them, NMC is able to provide tax and accounting services in the USA, Europe and almost the entire world.

In particular, the Moores Rowland Network, of which NMC is a key member, has been established with the Asian countries listed below, enabling the provision of highly detailed services.

Moores Rowland CPAs 衆智聯合会計士事務所

Taiwan Certified Public Accountant

Jason Liu

Shu-chi United Public Accountants was established in 1987. In Taiwan, the firm has offices in Taipei, Taoyuan, Hsinchu, Taichung and Kaohsiung and provides various accounting and tax services.

As a company providing global services, Jason Liu is a Taiwanese member firm of Praxity (Praxity AISBL)the seventh largest accounting firms association in the world.

Established in 2006, their team dedicated to Japanese corporations under the leadership of Liu CPA is composed of accountants and staff with a great deal of experience in various industries and knowledge of financial auditing, tax auditing and construction office management, facilitating the provision of services and consultation services in Japanese. In order to meet the needs of clients, NMC provides not only corporate outsourcing services, such as bookkeeping, accounting and taxation, but also consultancy services necessary for Japanese companies to carry out their business in Taiwan.

They have built a long-standing relationship of trust with us, NMC, through the dispatch of staff to each other.

Shu-chi United Public Accountants was established in 1987. In Taiwan, the firm has offices in Taipei, Taoyuan, Hsinchu, Taichung and Kaohsiung and provides various accounting and tax services.

As a company providing global services, Jason Liu is a Taiwanese member firm of Praxity (Praxity AISBL)the seventh largest accounting firms association in the world.

Established in 2006, their team dedicated to Japanese corporations under the leadership of Liu CPA is composed of accountants and staff with a great deal of experience in various industries and knowledge of financial auditing, tax auditing and construction office management, facilitating the provision of services and consultation services in Japanese. In order to meet the needs of clients, NMC provides not only corporate outsourcing services, such as bookkeeping, accounting and taxation, but also consultancy services necessary for Japanese companies to carry out their business in Taiwan.

They have built a long-standing relationship of trust with us, NMC, through the dispatch of staff to each other.

Main services

- Auditing (financial and tax audits)

- Accounting services (bookkeeping, monthly closing of accounts, review and support for preparation of consolidated financial statements).

- Tax services (various corporate and individual tax procedures, business tax calculations, withholding services on behalf of clients, etc.)

- Payroll outsourcing services

- Registration services (FIA applications, company incorporation, visa and other registration applications required for investment and expansion into Taiwan, etc.)

- Consulting and other services (tax consultation for transactions between Taiwan and the Mainland, etc.)

Moores Rowland (HK) CPA Limited

Director

Thomas Lee

Moores Rowland in Indonesia

Senior Advisor / CEO

James Kallman

Moores Rowland Singapore

Managing Partner

LEE Lee King

Bunchikij Co., Ltd. (Moores Rowland Thailand)

Managing Director

Pornchai Kittipanya-Ngam

Transfer Pricing Services

We analyze and advise Japanese companies on tax risks arising from intangible asset transactions such as provision of services and software royalties that Japanese companies face when expanding overseas.

We analyze and advise Japanese companies on tax risks arising from intangible asset transactions such as provision of services and software royalties that Japanese companies face when expanding overseas.

We support companies in their decision-making process by measuring the risk of transfer pricing correction.

In recent years, the risk of transfer pricing taxation has increased not only for large companies, but also for small and medium-sized companies.

A last-minute response, i.e., taking action only after taxation, will not eliminate double taxation in Japan and the destination country, and will result in damage to cash flow, which is the cornerstone of corporate management. For this reason, transfer pricing is a pressing issue for companies that have expanded overseas (including foreign corporations that have established operations in Japan). It is also unrealistic for companies with many overseas offices to deal with transfer pricing at one time.

We support companies in their decision-making process by measuring the risk of transfer pricing correction. This allows us to identify transactions and locations that should be prioritized and propose an efficient plan to reduce transfer pricing risk.

1. Risk Assessment

We support companies in their decision-making process by measuring the risk of transfer pricing correction.

In recent years, the risk of transfer pricing taxation has increased not only for large companies, but also for small and medium-sized companies.

A last-minute response, i.e., taking action only after taxation, will not eliminate double taxation in Japan and the destination country, and will result in damage to cash flow, which is the cornerstone of corporate management. For this reason, transfer pricing is a pressing issue for companies that have expanded overseas (including foreign corporations that have established operations in Japan). It is also unrealistic for companies with many overseas offices to deal with transfer pricing at one time.

We support companies in their decision-making process by measuring the risk of transfer pricing correction. This allows us to identify transactions and locations that should be prioritized and propose an efficient plan to reduce transfer pricing risk.

2. Policy Development

Harmful effects of independent documentation at overseas locations

Many countries, including China, require transfer pricing documentation to be prepared by the annual tax return filing deadline, and documentation of overseas offices is part of this requirement. However, if left to foreign offices, local accounting firms tend to prepare documents that show a higher level of profit for the local corporation in order to reduce tax risk in that country. While this is indeed effective to reduce tax risk there, it also increases the possibility that profit that should be allocated to Japan are allocated to the local country branch, causing the Japanese tax authorities to potentially see there a transfer pricing problem. Furthermore, if each foreign branch takes a different approach, it will be difficult to achieve consistency across the entire corporate group, which may result in a disadvantageous situation during tax audits in Japan. To prevent this problem, it is important to establish a transfer pricing policy by unifying the basic policy regarding pricing of foreign-related transactions within the company. As corporate groups become increasingly internationalized, a parent company-driven transfer pricing policy is considered essential to avoid taxation risks.

How to determine a transfer pricing policy

Identify foreign-related transactions

There are various types of foreign-related transactions, including inventory transactions, service transactions, royalty transactions and financial transactions. Some inventory transactions may be simple purchases and sales of raw materials, while others may be similar to contract manufacturing. The first step is to identify the foreign-related transactions carried out by the company, based on interviews with the persons in charge of each department of the company.

Analyze Risks and Review Price Calculation Methods

For each foreign-related transaction that has been identified through interviews, the functions performed by both parties to the transaction and the risks borne are analyzed, and the method of allocating the income from the foreign-related transaction to the related parties and the method of calculating the arm’s length price are examined.

Formulate Operating Rules

In accordance with the method of calculating the arm’s length price determined after the study, the company will formulate internal operating rules. This process cannot be completed by the accounting staff alone, but requires a company-wide consensus, including the business units, and in some cases, it may be necessary to reconsider the performance evaluation methods used by overseas offices.

Prepare a Transfer Pricing Policy Document

The transaction policy and internal operating rules compiled so far should be put together in writing so that they can be immediately submitted to the inspector in the event of a transfer pricing tax audit. A well-documented transfer pricing policy document, backed up by solid factual findings, can be expected to give the company an advantage in a transfer pricing investigation.

3. Documentation

Support for Proper Transfer Pricing Documentation Based on Legal Requirements

Under the transfer pricing taxation system, it is a legal requirement to document the details of transactions with related foreign companies and to submit this documentation promptly upon request by an inspector.

Although there are legally required items to be included in the documentation, it is usually very difficult for a taxpayer to complete all of these items on their own.

We provide services to assist companies with transfer pricing documentation.

Transfer pricing documentation process

STEP 1. Preliminary meeting

We first conduct a preliminary meeting to obtain a broad understanding of the case and identify the companies to be analyzed for transfer pricing.

Since the man-hours required for transfer pricing documentation can vary greatly depending on the number and complexity of transactions with related foreign companies, this would allow us to provide an estimation of the cost.

STEP 2. Estimate

The complexity of the transactions is evaluated, and the documentation costs are individually estimated.

STEP 3. Fact-finding interviews, confirmation of the contents of contracts, etc.

After contract finalization, we will conduct interviews to confirm the actual status of the transactions with related foreign parties between your company and foreign affiliates. Ideally, we will interview not only the person(s) in charge of accounting, but also the persons in charge of these transactions in each department in order to uncover their true nature. Since unexpected risks may come to light, we will carefully and meticulously conduct interviews, paying close attention to even the most trivial details.

A higher degree of accuracy in our fact-finding word can be achieved if we are allowed to visit the factories or the overseas subsidiary to interview the local persons in charge.

STEP 4. Preparation of factual analysis reports and matching of contents

Fact-finding interviews are a step toward selecting comparator companies. If there are any factual errors or other inaccuracies here, it will affect all subsequent work, which is inefficient.

We compile what we have heard into a factual analysis report to ensure that there are no errors or shortcomings in the factual confirmation and to provide efficient documentation.

STEP 5. Functional and risk analysis, determination of the transfer pricing calculation method

Based on the results of the fact-finding work, the functions performed and risks borne by both parties to the transactions with foreign related parties are considered. In most cases, the company analyzed as performing a simpler function and bearing less risk is the company to be verified.

In parallel with the selection of the companies to be verified, the transfer pricing calculation method is also determined. The transfer pricing calculation method is legally regulated under the transfer pricing taxation system, so it is necessary to select the method that best fits the case out of the legally permitted methods.

STEP 6. Selection of comparator companies

Independent companies that perform similar functions and bear similar risks to the company selected for verification are selected as comparator companies. This process involves benchmarking tests using the same public company financial databases used by many taxation authorities in Japan and elsewhere. The most common method is to first identify comparator companies using quantitative indicators, then narrow down the list through qualitative analysis to determine the final comparator companies, and use statistical methods to calculate the range of operating margins of these companies.

STEP 7. Drafting of the final report and discussion of its contents

The (preliminary) results of the selection of comparator companies and benchmarking of profit margins based on functional and factual analysis are presented. We will explain our reasons for our selection of comparator companies, including our reasons for not choosing other companies. We will also ask for your company’s opinion before finalizing the report.

STEP 8. Final delivery

The final report is delivered, with corrections made if necessary. The whole process takes approximately three to four months.

The above is the full range of transfer pricing documentation services, but depending on the level of progress your company has made in transfer pricing, we can also provide benchmarking services only, for example, so please contact us for more details.

4. Advance Pricing Arrangement(APA)

What is Advance Pricing Arrangement (APA)?

Under the transfer pricing taxation system, it is a legal requirement to document the details of transactions with related foreign companies and to submit this documentation promptly upon request by an inspector.

Although there are legally required items to be included in the documentation, it is usually very difficult for a taxpayer to complete all of these items on their own.

We provide services to assist companies with transfer pricing documentation.

For transfer pricing inquiries

JC Tax Company / Transfer Pricing Desk

Taketsugu Osada

For transfer pricing inquiries

JC Tax Company / Transfer Pricing Desk

Taketsugu Osada

Contact us online

Contact us online